")

What is our best guess of what tax law changes could be coming with the new Trump Administration? We outlined what could happen under Trump based on the sources that are cited at the end of this article.

IRS Workforce

According to articles, roughly 6,000-6,700 IRS employees have been laid off. Those fired include:

- Revenue Agents

- Customer Service Representatives

- IT Workers

- Appeals Specialists

- Most of the workers laid off audited tax forms and collected arrearages

IRS employees have been offered a deal that would compensate them for the layoff, however, those who accepted the deal will have to stay on the job through May 15, 2025. IRS workers with positions within Taxpayer Services, Information Technology, and Taxpayer Advocate Services cannot be placed on leave until May.

The layoff affected probationary employees with roughly one year or less of service at the agency, most of which were from compliance departments.

Trump administration intends to lend IRS workers to the DHS to assist with immigration enforcement.

Reports suggest the terminations will target mostly new and newly promoted employees, with half of the cuts hitting an office known as the Small Business/Self-Employed (SBSE) Division.

Sources

- Elon Musk’s DOGE Begins IRS Audit. What to Know – Newsweek

- IRS fires 6,000 employees as Trump slashes US government | Reuters

- The IRS is firing thousands of workers. Will it affect your tax refund?

- Trump administration will cut thousands of jobs at Pentagon and IRS

Tax Refunds

Multiple sources have suggested: everyone file electronically and accurately to receive a refund as soon as possible. As long as return is accurate and it is filed electronically, refunds are expected to be received within 3 weeks, sooner if direct deposit is chosen.

If you file by mail, refunds are expected withing 6-8 weeks from the date IRS receives the return. If manual reviews are required, even longer wait time.

Source

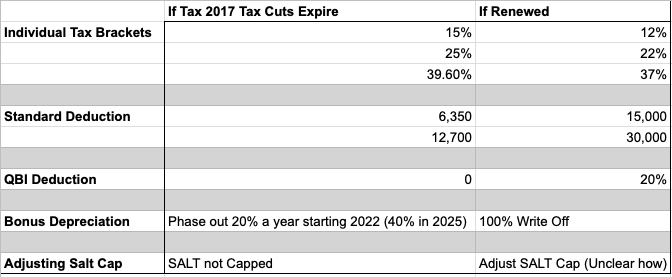

Trump Administration Tax Changes

Permanent TCJA policy:

- Corporate income tax rate of 21%

- Business interest expense limitations

- Certain international provisions (scheduled to incur rate changes)

- Capitalization and Amortization of R&D

Source

Proposals:

- Eliminate Federal Income Tax, replace with tariffs

- “We’re going back to the old days. No income tax, just tariffs. It worked before, and it’ll work again” “The IRS is a disaster. We don’t need it. Tariffs will fund everything we need and more.” – Donald Trump, 1/25

- Lower Rates of Audits

- Simplifying the Tax Code

- Increase SALT Cap or remove SALT Cap

- Currently capped at $10,000

- Either remove cap or double it to $20,000 (MFJ and MFS only)

- What it means? Can deduct a max of 20k on property taxes, state taxes, sales tax, local income tax. Or no limit on the amount deductible.

- Reduce taxes on U.S. Citizens living abroad

- Reduced corporate tax rate to 15% for companies making products in US, 20% for all other corporations

- Taxation of large, private university endowments

- Exempt income from overtime, tips, social security benefits

- Favors a return to 100% bonus depreciation for qualified property

- Favors expanded R&D tax credits, unclear as to whether this refers to Section 41 credits or a reversal of Section 174 capitalization

- Interest deductions on automobile loans for vehicles manufactured in the US

- Inflation Reduction Act; Modification and/or repeal – TBD.

Sources

- Trump’s back in office — here’s what to expect for your taxes in 2025 and beyond

- Trump’s 2025 Tax Plans: Experts Weigh in on What Could Happen, What’s Wrong With Trump’s Plan to Abolish Income Tax | Kiplinger

- Potential tax law changes in the new Trump Administration – BPM

SALT Cap

It is generally believed that the SALT deduction cap will not be fully repealed. The cap may be higher, or other changes can be implemented. Some options already on the table include:

- Doubling the SALT deduction to $20,000 for couples filing joint, $10,000 Single

- Triple SALT deduction cap to $30,000 for couples filing joint, $15,000 for other filers

- Greatly increases SALT deduction cap to $200,000 for couples, $100,000 for other filers

AMT

It is unclear as to how Congress will handle the expiring AMT.

Pass-through Entities

Unless the SALT deduction cap is fully repealed, it should be expected that the state workarounds involving passthrough entities will continue to exist

As per the Press Secretary, the President’s priorities are focused on the renewal of the 2017 middle class tax cuts, adjusting the SALT cap, eliminating special tax breaks for billionaire sports team owners, and closing the carried interest deduction loophole.

2025 IRS Changes; Confirmed:

Standard Deduction Increases:

- Single: $14,600 🡪 $15,000, $400 Increase

- MFJ: $29,200 🡪 $30,000, $800 Increase

- HOH: $21,900 🡪 $22,500, $600 Increase

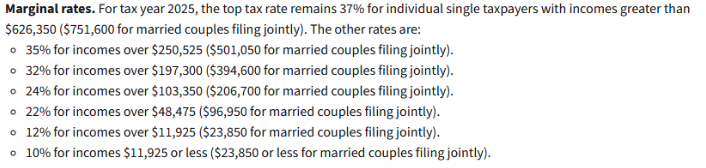

Marginal Tax Rates:

- 37%

- Single: Income > $626,350

- MFJ: Income > $751,600

- 35%

- Single: Income > $250,525

- MFJ: Income > $ 501,050

- 32%

- Single: Income > $197,300

- MFJ: Income > $394,600

- 24%

- Single: Income > $103,350

- MFJ: Income > $206,700

- 22%

- Single: Income > $48,475

- MFJ: Income > $96,950

- 12%

- Single: Income > $11,925

- MFJ: Income > $23,850

- 10%

- Single: Income > $11,925

- MFJ: Income > $23,850

Alternative Minimum Tax Exemption Amounts

Exemption amount for unmarried individuals increases to $88,100 ($68,650 for married individuals filing separately) and begins to phase out at $626,350. For married couples filing jointly, the exemption amount increases to $137,000 and begins to phase out at $1,252,700.

Earned Income Tax Cedits

For qualifying taxpayers who have three or more qualifying children, 2025 maximum Earned Income Tax Credit amount is $8,046.

Qualified Transportation Fringe Benefit

Monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking rises to $325

Health Flexible Spending Cafeteria Plans

- Dollar limitation for employee salary reductions for contributions to health flexible spending arrangements rises to $3,300. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount rises to $660.

- Medical savings accounts Participants who have self-only coverage the plan must have an annual deductible that is not less than $2,850, but not more than $4,300.

The maximum out-of-pocket expense amount rises to $5,700.

Family Coverage

For family coverage, the annual deductible is not less than $5,700; however, the deductible cannot be more than $8,550. For family coverage, the out-of-pocket expense limit is $10,500.

- Foreign earned income exclusion. The foreign earned income exclusion increases to $130,000

- Estate tax credits. Estates of decedents who die during 2025 have a basic exclusion amount of $13,990,000.

- Annual exclusion for gifts increases to $19,000

- Adoption credits. The maximum credit allowed for the adoption of a child with special needs is the amount of qualified adoption expenses up to $17,280.

Source

IRS releases tax inflation adjustments for tax year 2025 | Internal Revenue Service

2025 Tax Return Changes:

Standard Deduction:

-

- Single, Married, filing separate: increase standard deduction +400, 2025 standard deduction = $15000

- MFJ: $30,000

- HOH: $22,500

Tax Brackets:

Alt Min Tax:

-

- Single: Exemption $88,100

- MFS: $68,650

- Phase out begins at $626,350

- MFJ: $137,000

- Phase out begins at $ $1,252,700

EIC:

3+ Qualified Children = $8,046

Qualified Transportation Fringe Benefit:

Limitation for monthly qualified parking = $325

Health Flexible Spending Cafeteria Plans:

For the taxable years beginning in 2025, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements rises to $3,300, increasing from $3,200 in tax year 2024. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount rises to $660, increasing from $640 in tax year 2024.

Medical Savings Accounts:

For tax year 2025, participants who have self-only coverage the plan must have an annual deductible that is not less than $2,850 (a $50 increase from the previous tax year), but not more than $4,300 (an increase of $150 from the previous tax year).

The maximum out-of-pocket expense amount rises to $5,700, increasing from $5,550 in tax year 2024.

For family coverage in tax year 2025, the annual deductible is not less than $5,700, increasing from $5,550 in tax year 2024; however, the deductible cannot be more than $8,550, an increase of $200 versus the limit for tax year 2024. For family coverage, the out-of-pocket expense limit is $10,500 for tax year 2025, rising from $10,200 in tax year 2024.

Foreign Earned Income Exclusion:

For tax year 2025, the foreign earned income exclusion increases to $130,000, from $126,500 in tax year 2024.

Estate Tax Credits:

Estates of decedents who die during 2025 have a basic exclusion amount of $13,990,000, increased from $13,610,000 for estates of decedents who died in 2024.

Annual exclusion for gifts increases to $19,000 for calendar year 2025, rising from $18,000 for calendar year 2024.

Adoption Credits:

For tax year 2025, the maximum credit allowed for adoption of a child with special needs is the amount of qualified adoption expenses up to $17,280, increased from $16,810 for tax year 2024.

Source