")

This is HUGE! A recent use tax audit of a current client has resulted in a revelation concerning what I perceive to be ever-increasing exposure for sales and use tax enforcement audits against California residents and businesses, and against out of state retailers.

For the past couple months, I have been receiving ever-increasing frantic phone calls from out of state retailers that ship into California with concerns surrounding inquiries from the California Department of Tax and Fee Administration (“CDTFA”), formerly known as the Board of Equalization, (“BOE”), indicative of a potential or pending sales tax audit. These inquiries stem from the agencies concern that out of state retailers could be liable for collecting and remitting California Sales tax where goods were being shipped to California residents and businesses.

This week, the sweetest couple came into my office for a consultation, and they were absolutely panicked by a letter they received from the CDTFA. The couple is retired and living on social security. Before receiving the redacted version of the letter below from the CDTFA the couple represented to me that they had absolutely no idea that they were responsible for use tax on goods purchased outside California without the vendor collecting and remitting California sales tax. It has been my experience that most California residents are not aware of the concept of use tax so this did not surprise me. To that end, let me start with some use tax basics before telling the rest of this story.

Use Tax Basics:

Simply stated, if you purchase a tangible good outside California, ( i.e., another State or even from offshore in certain circumstances) for use within California, as a California resident, you are required to self-assess California use tax which is basically equal to the sales tax you would have paid had you purchased the good from a California retailer.

In general, California businesses must pay use tax on purchases from out of state retailers, whether the product is ordered by telephone, via the Internet, by mail order, or ordered in person, where both of the following conditions apply:

- The out of state seller did not collect California sales or use tax which can be verified by examining the purchase invoice/receipt to determine if the sales tax was added.

- The California business consumes, utilizes, gives away and/or stores, the item purchased out of state in California. Note that these same items would have been charged sales tax if they had been purchased from a California retailer.

Not all items purchased are subject to sales tax. For example, food for human consumption such as barbeque sauce and ice cream is not subject to sales tax. Moreover, electronically downloaded software, music, and games are not subject to tax if no tangible storage media is purchased at the same time.

The man of the house, from the couple I was discussing above, had a passion for photography. He enjoyed doing photography as a hobby, taking many pictures of his travels, daily life, etc. Recently, he decided to order photography equipment from Amazon and a drafting table directly from an out of state retailer that sold used camera equipment over the internet. He placed the order, as he had in several years past, admitting that he favored internet purchases because the items obtained over the internet, including shipping costs, were less expensive than he could obtain from local merchants. Unbeknownst to my client, is the use tax exposure created where his perceived savings related to an out of state vendor not collecting and remitting California sales tax?

Evidently, the out of state retailer from which he purchased the drafting table had their truck stopped as it was entering California at the border at an Agricultural check station run by the California Department of Agriculture (“CDoA”). The CDoA routinely obtains a document from each truck driver stopped at the border known as a “Bill of Lading”, which includes information on the items being shipped, including the value of the items, who was shipping the items, where the items were being shipped to, the price paid per each item shipped and whether California sales tax had been charged on these items by the out of state vendor. The information collected by the CDoA, concerning the $800 drafting table my client had purchased, was evidently forwarded to a special unit of the CDTFA.

Apparently, the State of California’s is taking this information collected at the border by the CDoA and methodically, reaching out to any out of state vendor that is shipping into California and inquiring with the out of state vendor whether they are collecting or remitting sales tax on the goods shipped into California. My suspicion is this unit does a quick check to see if the vendor has registered with the CDTFA to collect and remit California sales tax, and, if they have not, the vendor is sent an inquiry letter. I suspect this is one-way the CDTFA is currently identifying targets for possible sales tax enforcement action where the out of state vendor is shipping into California.

The good news is that according to the CDTFA’s website, it takes more for an out of state retailer to have nexus with the state of California than simply selling into California via common carrier. The CDTFA has been emboldened by the outcome of “Amazon vs. The State of California” in 2012. As a result of this litigation, Amazon has been subsequently forced to collect and remit California sales tax because it maintains distribution facilities within California which the court found was sufficient to establish California sales tax nexus.

The above revelations seems to explain why I have been getting so many contacts from all over the country by out of state retailers that are receiving letters from the CDTFA asking them whether they have a duty to collect and remit sales tax. After evaluating an out of state retailer’s exposure for this issue, I have been putting many of them in a special California Voluntary Disclosure Program for out of state Businesses and Taxpayers, as a way to avoid criminal prosecution, limit the number of past tax years at issue and limit penalties and interest where warranted by each client’s specific facts and circumstances.

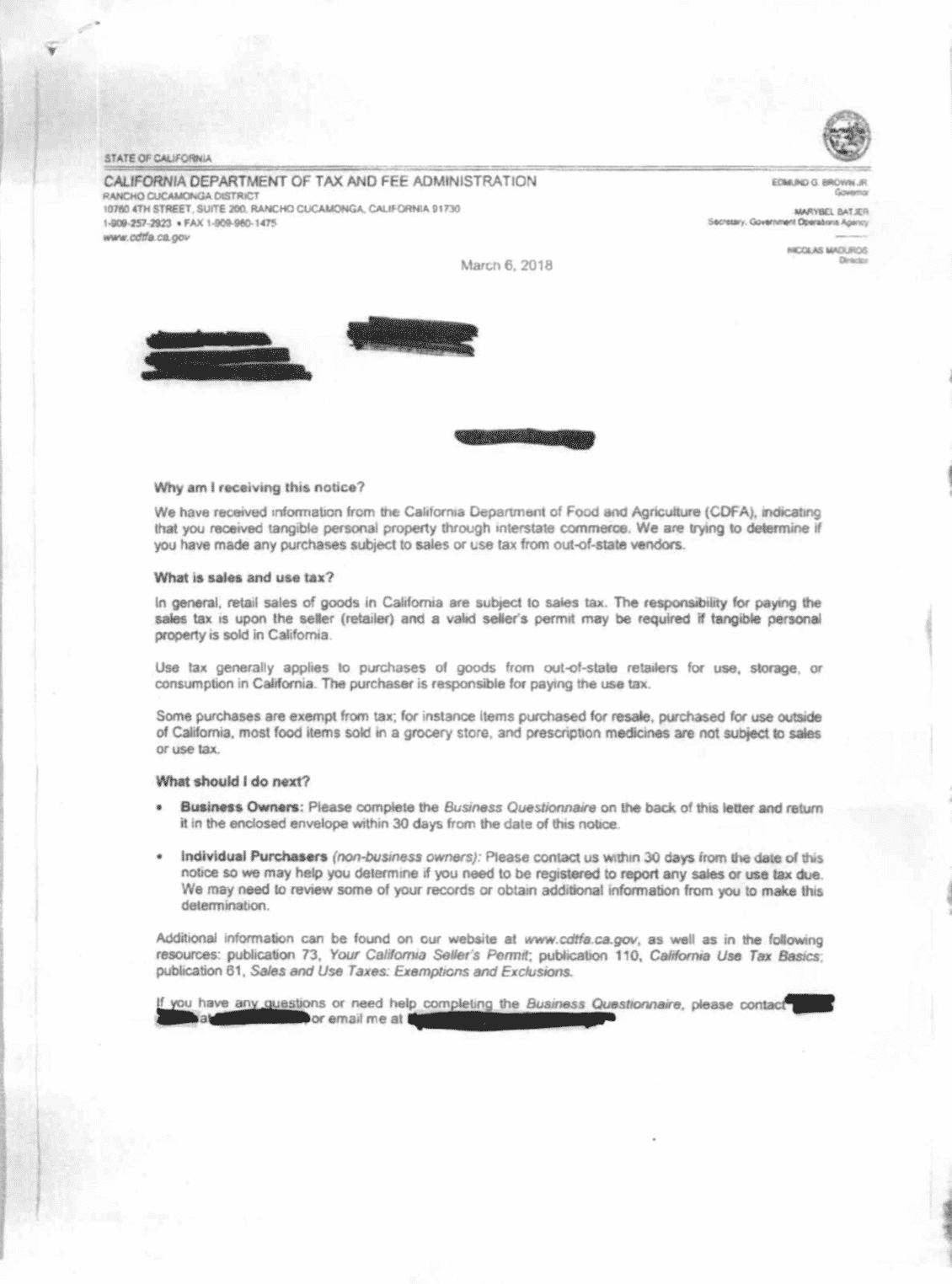

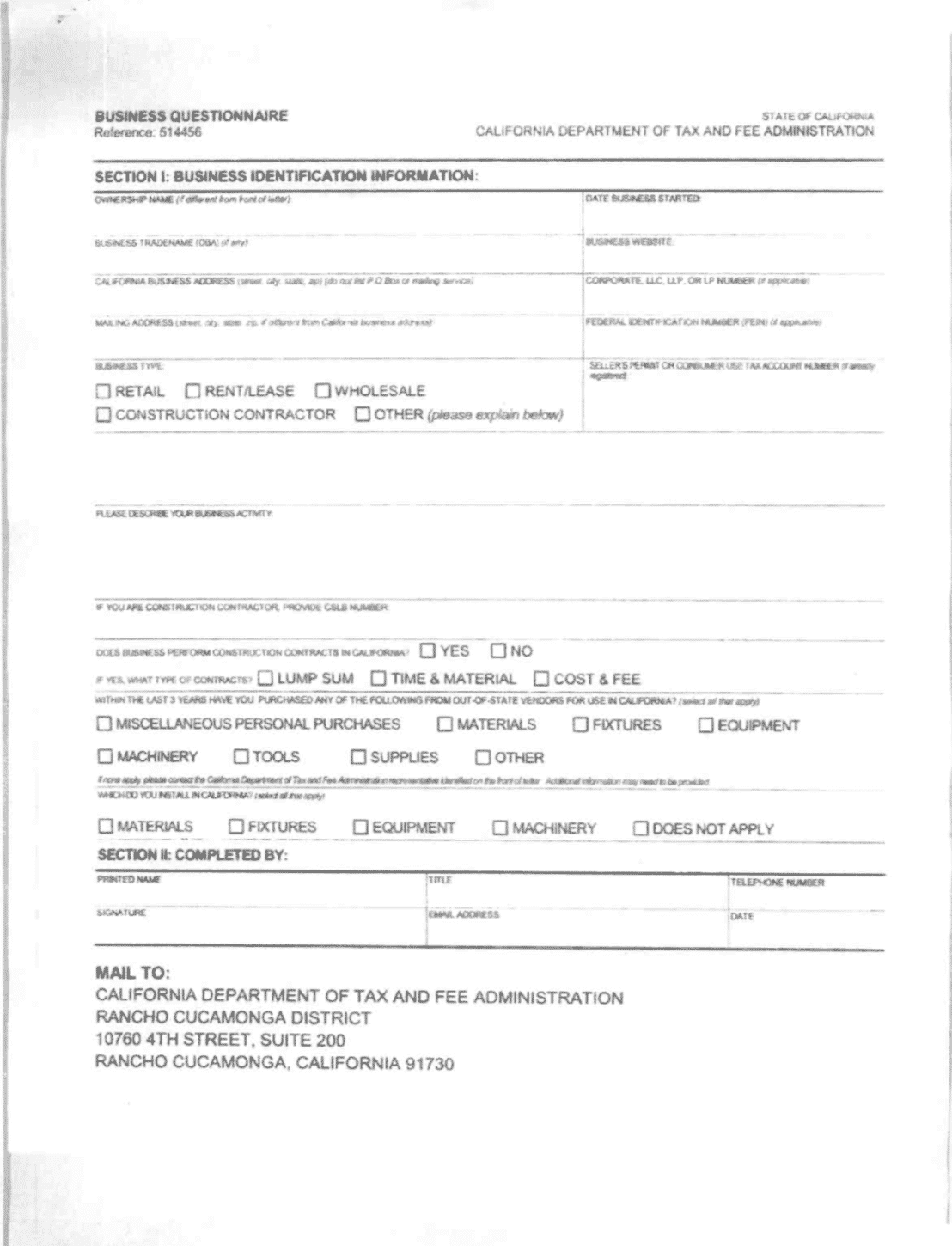

A great deal of what I wrote about above I deduced when I spoke at length to a member of the Special Unit of the CDTFA that had opened a use tax inquiry against my horrified clients. Evidently, there are 12 agents in this special unit each writing 200 inquiry letters a month. The agent stated that after this unit had attempted to secure sales tax from the out of state vendor unsuccessfully, usually because a determination was made that the out of state vendor did not have enough contact with state of California to establish sales tax nexus, the agents then attempted to collect use tax from the buyer that received the goods via the redacted inquiry letter supplied below. Page two of the inquiry letter leads me to believe that this may be another way of identifying California businesses that owe use tax or that should be collecting and remitting California sales tax or may be part of California’s underground economy. The term “underground economy” refers to individuals and businesses that often deal solely in cash, do not supply receipts, and are known to use schemes to conceal their illegal activities and often evade state income and sales tax liability by misleading California licensing, regulatory, and taxing agencies. The underground economy is associated with tax evasion, tax fraud, payments to employees under-the-table, and off-the-book sales and the use of skimmer programs to fraudulently understate sales and adjust costs of goods sold to attempt to hide it.

A common scheme that routinely blows up on California resident’s is to purchase a vehicle, boat or aircraft in another state in an attempt to avoid California sales tax. If you purchase a car in Arizona, for example, the out of state vendor cannot charge you Arizona sales tax because you are not a resident of that state. Moreover, the out of state vendor will not ordinarily be required to collect and remit California sales tax because they do not have sufficient contacts with California to warrant sales tax nexus. However, when you drive your brand-new vehicle into California, you are legally required to calculate and voluntarily remit California use tax, this goes for boats and aircraft as well. California is known to obtain information for vehicle, boat and airplane registrations, from other state agencies, the Department of Motor Vehicles for example, to see if you have paid California sales or use tax on the out of state purchase. If you did not pay sales tax on the out of state purchase, the CDTFA will eventually access you use tax, along with penalties and interest. Unfortunately, if they can prove that you purposely evaded use tax on the out of state acquisition, you have exposure for a California tax crime called “Sales Tax Evasion”.

Under the California Revenue and Taxation Code, any person or business that intentionally fails to report the assessment and fails to subsequently make payment of legally incurred sales and use taxes is guilty of sales tax evasion and can be faced with monetary fines and/or incarceration.

Examples of sales tax evasion include,

- A California retailer that collects sales tax from customers and intentionally fails to report and remit the sales tax they appropriately or inappropriately collect.

- Retailers that intentionally fail to report all taxable retail sales on which sales tax is due especially where steps are taken to mislead the taxing authorities.

If after learning of your exposure and the fact that you have liability for use tax, in the absence of any type of inquiry with the state of California, there are two ways to handle the situation. You can either remit use tax annually on your California income tax return by including the goods purchased from out of state retailers where you were not charged California sales tax or you can remit the use tax directly through the CDTFA website as follows:

- Use the registration link on the old BOE website at https://www.boe.ca.gov/

- Chose the pay use tax, lumber assessment and/or prepaid MTS surcharge on one-time purchases option.

- Read the Declaration of Intent and hit “Accept”

- Follow the directions from there after completing the Preparer User Id Registration.

- Make electronic payment.

If you now realize you have use tax owed for prior tax years, an amended California income tax return may be in order. Note that California technically has a 20-year collection statute and no real limitation how many tax years it could go back and demand use tax, but common wisdom in the profession is that three tax years in total should be sufficient to start. One way of attempting to limit your civil and potential criminal exposure is to make use of California’s Voluntary Disclosure Program (“CVDP”) for in-state residents in order to attempt to limit the number of tax years, civil and criminal penalties and interest that could potentially apply, but this program cannot be entered into if you have already received the inquiry letter below and should not be entered without obtaining qualified legal counsel to make sure you understand the full ramifications and civil and criminal tax exposure before entering the CVDP. If you received the inquiry letter below I suggest you prudently obtain tax counsel (an Attorney – NOT a CPA) to intervene on your behalf and make sure there are no misunderstandings regarding your prior knowledge of the requirement to remit use taxes and the associated exposure for sales tax evasion no matter how seemingly remote.

My clients were rightfully frightened and extremely worried that the state of California was going to go back through all their records and potentially incriminate them for use tax liability at best and for sales tax evasion at worst. It still amazes me that the $76 dollars of use tax on an $800 out of state purchase was enough for the state of California to fire off the inquiry below. However, when I approached this special unit on behalf of my client, whom I refused to identify until I received some assurances on how the matter would be resolved, the agent stated they do not ordinarily tell the inquiry target this information. They ominously state in the inquiry letter that because they have received information from the California Department of Agriculture you may owe use tax and instructs the inquiry target to look into the matter and then call the CDTFA via the number listed on the letter. It was to my disbelief when I learned this matter was being handled as an actual correspondence audit. Each inquiry letter has a specific ID that identifies each inquiry target.

After the agent helped me reassure my clients they were not being criminally investigated, my client’s biggest concern was “How many years can they do this to us?” Sadly, in my opinion, they can seemingly go back indefinitely. Luckily, I was able to negotiate with the CDTFA and bring it down to 3 years of use tax even though she indicated she could easily go after 8 years of use tax. In exchange for positively identifying my clients and agreeing to work with the agent to resolve the inquiry, the auditor stated that she wasn’t interested in any Amazon purchases because, since the 2012 litigation, Amazon routinely now applies sales tax to 98% of purchases shipped into California. I inquired with the agent whether my clients should utilize the CVDP for in- state residents to limit their exposure, and she stated that would create an issue with an entirely different department and her inquiry would not go away in the meantime. She then represented that the inquiry letter sent to my clients effectively barred them from entering the CVDP as well.

Phone 800-681-1295 Mobile 714-514-2642 Email [email protected] Website https://klasing-associates.com/ |

| Satellite locations Los Angeles, San Bernardino, Santa Barbara, Panorama City & Oxnard. |

| Skype David.Klasing |

Virtual Office Tour (best if watched full screen) Firm Overview

Send Files To Me Securely Here

https://spaces.hightail.com/uplink/TaxLawOfficesofDavidWKlasing

Here is a link to our YouTube channel: click here!